Peter Smith

Peter Smith

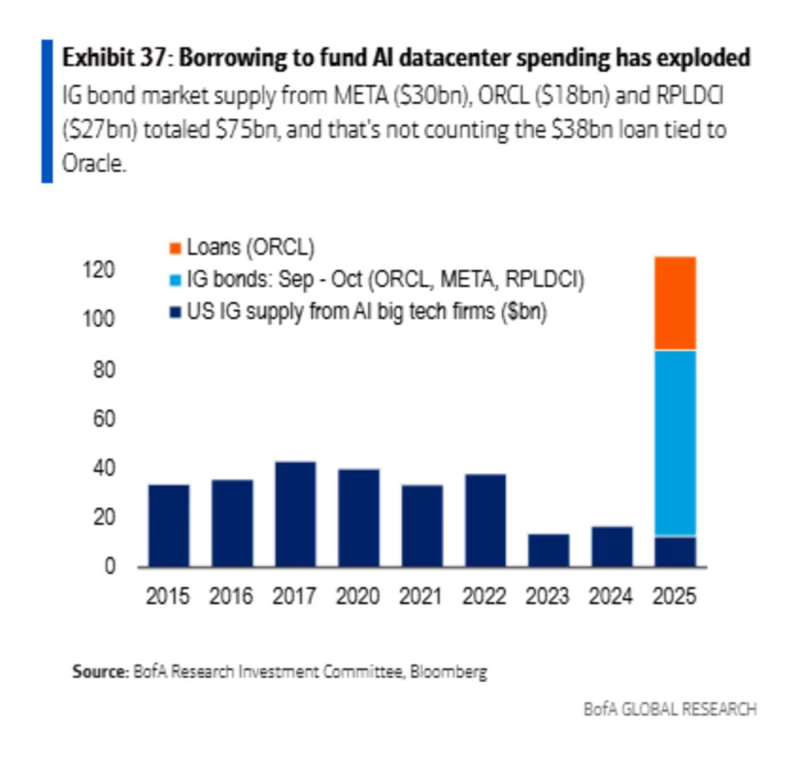

⬤ Bank of America's latest analysis shows large tech companies ramping up borrowing to pay for AI infrastructure. The five hyperscalers together issued $121 billion in debt this year, four times their average annual debt over the past five years. The chart tracks how investment-grade bond supply and loan activity tied to AI datacenter construction have jumped sharply, pushed by rising capital demands and longer deployment schedules.

⬤ The visualization shows 2025 borrowing sitting well above historical patterns. Investment-grade bond issuance from META, ORCL, and RPLDCI hit $75 billion, not counting a separate $38 billion Oracle loan, putting total funding near record territory. U.S. investment-grade supply from AI-focused big-tech firms stayed steady from 2015 through 2023, ticked up in 2024, then shot higher in 2025. AI infrastructure supply jumped more than 1,000% from 2024 to 2025, while datacenter capex climbed 53% year over year to $134 billion in Q1 alone.

⬤ Hyperscalers are now leaning on debt instead of operating cash flow to support AI expansion. IBM CEO Arvind Krishna pointed out the return challenge, noting that $8 trillion in capex would need $800 billion in annual profit just to cover interest, with infrastructure needing replacement every five years. Bank of America warns that rapid debt-funded AI build-outs may create an "air pocket," though it stops short of calling it a bubble. The bank forecasts just 4% upside for the S&P 500 in 2026, well below Deutsche Bank's 17% projection. The top 10 S&P 500 companies now make up 40% of the index's total market cap.

⬤ The shift toward debt-financed AI spending brings wider implications for valuation, capital allocation, and market concentration. Rising capex, higher borrowing, and shorter infrastructure cycles point to tighter financial conditions as AI spending keeps scaling. These dynamics could reshape expectations around growth, margins, and long-term sustainability across the AI ecosystem and broader equity market.

Peter Smith

Peter Smith