Peter Smith

Peter Smith

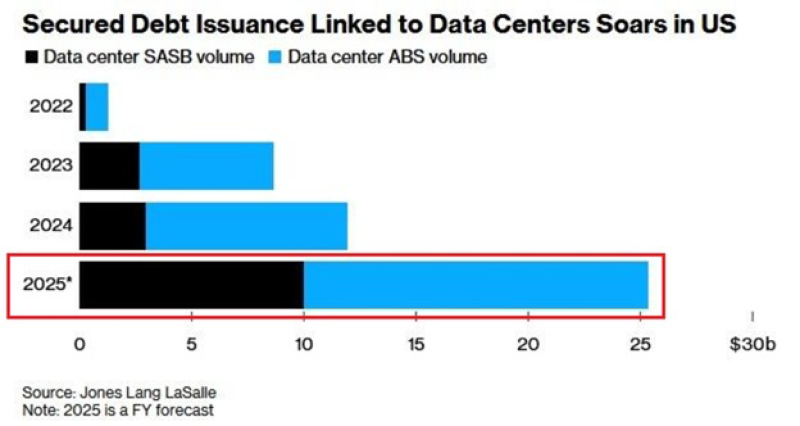

Something remarkable is happening in data center financing. We're witnessing what could be the biggest debt-raising year in US history, with 2025 projections climbing to $25.4 billion. The scale reflects a simple reality: artificial intelligence is hungry for computing power, and companies are racing to build the facilities that can deliver it.

AI Infrastructure Push Drives Record Borrowing

The Kobeissi Letter recently highlighted this explosive trend, pointing to a Jones Lang LaSalle chart showing the sector has gone from virtually no debt issuance in 2022 to a projected $25.4 billion in 2025.

That's a 112% year-over-year increase from 2024's $12 billion, and a staggering 1,854% surge since 2022. This fundamental transformation is driven almost entirely by AI demands, as hyperscalers, cloud providers, and private operators compete to build the massive compute capacity required for modern large language models and training clusters.

Chart Confirms Acceleration Across All Structures

Both SASB (Single-Asset, Single-Borrower) debt and ABS (Asset-Backed Securities) are climbing rapidly, with combined 2025 projections reaching nearly $30 billion. BofA estimates there's already $49 billion in data center ABS and CMBS in existence, creating an increasingly leveraged financing ecosystem around digital infrastructure.

Why the Debt Surge Is Happening Now

Several forces are converging to create this explosion:

AI hardware demand has reached historic highs, with GPUs and accelerators in short supply pushing operators to build faster. Next-generation AI data centers often need 200 to 600+ megawatts per site, driving massive upfront capital needs. Construction and land costs are climbing in key US markets where suitable sites are scarce. Despite higher interest rates, investor confidence remains strong because lenders view data centers as stable assets with clear long-term demand.

What This Means for the AI Ecosystem

The numbers reveal something crucial: AI progress is no longer constrained by algorithms—it's constrained by physical infrastructure capacity. Record debt issuance suggests AI build-outs will accelerate further in 2025, operators may take on higher leverage risks, power grid limitations will become critical, and the financing model is becoming more aggressive and complex.

Peter Smith

Peter Smith