Marina Lyubimova

Marina Lyubimova

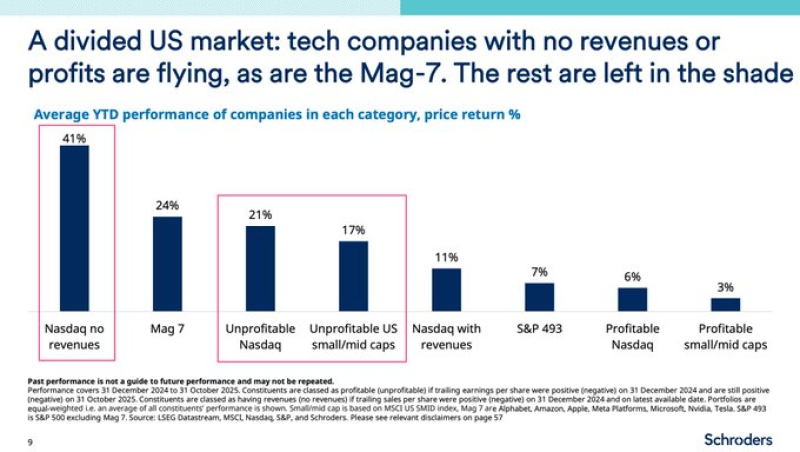

⬤ Schroders has published fresh performance numbers that show how polarised the US equity market has become in 2025. Nasdaq firms that still report no sales have leapt 41 percent since January - the seven largest tech stocks are up 24 percent. In contrast profitable businesses and the broad middle of the market have hardly budged, a sign that investors now reward sheer size plus future promises more than reliable earnings.

⬤ The surge centres on four areas - artificial intelligence hardware, quantum computers, space projects and new nuclear designs. Government policy is friendly but also investor appetite is hot - valuations in those niches have risen faster than most forecasters anticipated. Loss-making Nasdaq companies have climbed 21 percent - loss making small- and mid-capitalisation names have added 17 percent. Nasdaq companies that already generate revenue have managed only 11 percent, while the S&P 493 - the index without the mega tech names - has delivered 7 percent.

First-movers in AI, space, quantum as well as nuclear are facing demand that is stronger and earlier than expected, helped by Washington's push behind those themes.

⬤ The seven tech giants keep the lead because they own the basic inputs the AI economy needs - processing power, data or customer reach. Profitable Nasdaq companies outside that circle have gained 6 percent - profitable smaller and medium-sized firms have advanced 3 percent. Businesses that sit outside the AI-innovation wave find it hard to draw capital even when their balance sheets look healthy.

⬤ This divide matters - it shows that capital is rushing into speculative high growth names also dominant AI platforms while traditional industries are left aside. The market now moves on narrative themes instead of standard valuation yardsticks - the risks and the openings you face depend on which side of the split you stand.

Marina Lyubimova

Marina Lyubimova