Saad Ullah

Saad Ullah

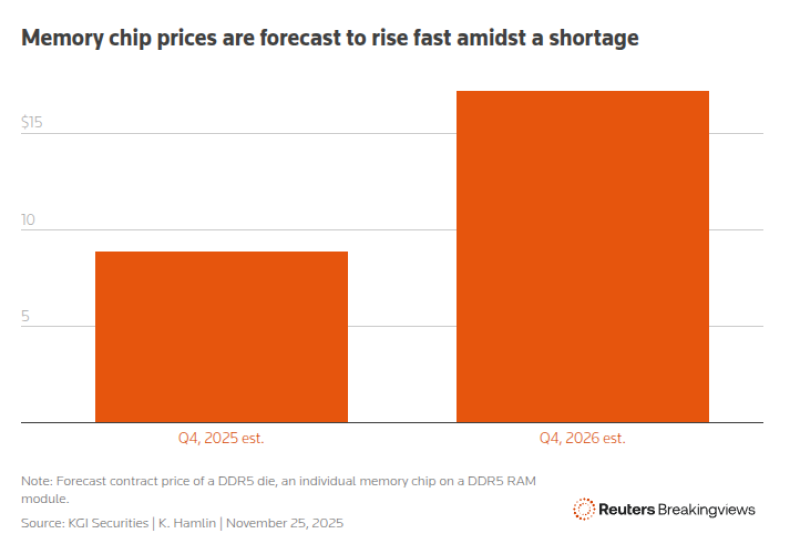

⬤ Memory manufacturers are bracing for steep DRAM price increases as AI infrastructure fundamentally changes the industry's economics. AI data centers are consuming high-speed memory at unprecedented rates, pushing suppliers like Micron (MU), Samsung, and SK hynix to pour more investment into high-bandwidth memory for AI accelerators. DDR5 contract prices are expected to climb from around $8 per chip in Q4 2025 to over $14 by Q4 2026—a 75% jump that underscores just how tight supply has become.

⬤ HBM has emerged as the most lucrative segment in the memory market, backed by multi-year contracts with major cloud providers that guarantee full absorption of everything manufacturers can produce. SK hynix, Samsung, and Micron can sell their entire HBM output years ahead of time. This shift is pulling wafer capacity away from DDR4 and DDR5 production, even as AI-driven demand for conventional server DRAM stays strong and proves fairly insensitive to price hikes. With fewer fabs making commodity DRAM and hyperscalers buying aggressively, contract prices keep climbing quarter after quarter.

⬤ Some DDR4 segments have already seen prices more than double in short windows, according to market trackers like TrendForce. This squeeze carries over from the previous memory downturn when DRAM makers slashed spending after taking major losses. Manufacturers are being careful not to overproduce generic DRAM again, keeping supply tight and prices elevated through late 2026.

⬤ The pricing shift has major implications across the semiconductor sector since memory represents a core cost in AI servers and data-center equipment. If DRAM and HBM prices keep rising at this pace, profitability for Micron, Samsung, and SK hynix could get a serious boost, while hardware makers face ongoing cost pressure. With supply constrained, demand holding firm, and capital focused on HBM, the market looks set for continued tightness and upward price momentum well into 2026.

Saad Ullah

Saad Ullah