Marina Lyubimova

Marina Lyubimova

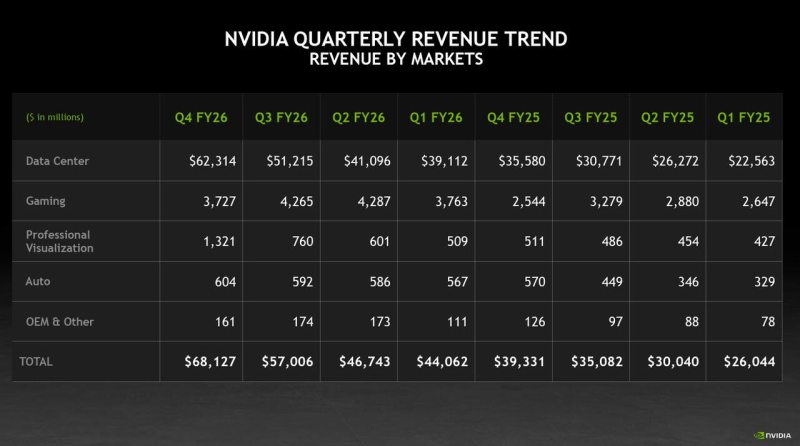

Nvidia just delivered one of the most impressive quarterly performances in semiconductor history. The company reported total revenue of $68.13 billion, up 73% year-over-year, while adjusted earnings per share of $1.62 topped the consensus estimate of $1.53. According to Lance Roberts, Nvidia's top-line performance outpaced forecasts by roughly $2.2 billion - a gap that reflects just how fast AI spending is accelerating.

Data Center Revenue Hits $62.31B, Up 75% Year-Over-Year

The numbers tell a clear story. Nvidia leads the AI semiconductor stack as hyperscalers and enterprises pour capital into compute infrastructure - and those dollars are showing up directly in the data center segment. At $62.31 billion, it came in well above the $60.36 billion estimate. Networking revenue more than tripled year-over-year to $10.98 billion, blowing past the $9.02 billion projection. Compute revenue climbed 58% to $51.33 billion.

Nvidia's performance outpaced forecasts by approximately $2.2 billion, underscoring the continued strength of its core business, particularly in AI-driven data center demand. - Lance Roberts

Gaming revenue came in at $3.73 billion, up 49% year-over-year but slightly below the $4.01 billion estimate. Professional Visualization was a bright spot at $1.3 billion, more than doubling from $511 million a year earlier. Automotive posted $604 million, up 6% but narrowly missing forecasts. Nvidia continues expanding its software ecosystem, recently launching Nemotron 3 Nano on Amazon Bedrock - signaling ambitions well beyond hardware.

AI Infrastructure Demand Shows No Signs of Slowing

The broader picture is straightforward: AI workloads are driving an infrastructure build-out at a scale the industry hasn't seen before. Data center revenue now makes up the dominant share of Nvidia's total sales, and it's growing fast.

With hyperscalers committing hundreds of billions to AI compute, GPU breakthroughs like TurboDiffusion - which cuts video generation time from 184 seconds to just 19 - are only reinforcing Nvidia's position at the center of that spending. The company's ability to beat estimates by this margin, quarter after quarter, suggests the AI investment cycle still has considerable runway ahead.

Marina Lyubimova

Marina Lyubimova