Eseandre Mordi

Eseandre Mordi

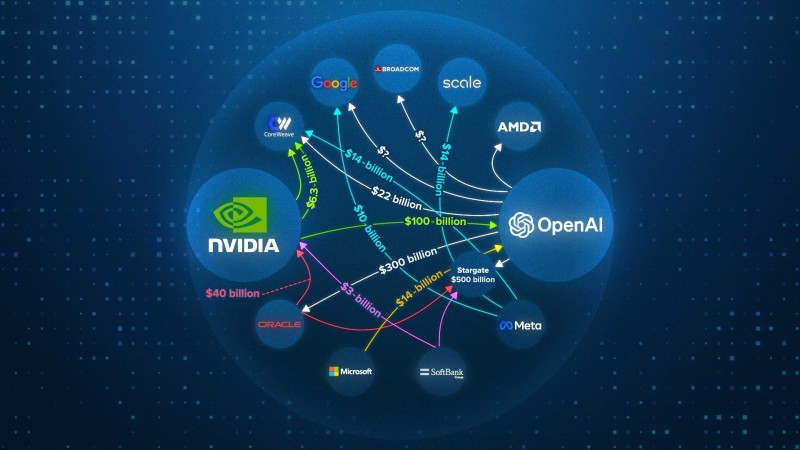

⬤ The AI sector is pulling in roughly $60 billion in revenue this year while torching close to $400 billion. That massive shortfall is being covered through debt, off-balance-sheet tricks, and circular funding loops. Recent disclosures reveal just how tangled up the major AI players have become—Nvidia, OpenAI, cloud giants, and infrastructure firms are all deeply interconnected in a tight financial web.

⬤ CoreWeave offers a prime example of how these deals work. The company uses Nvidia-backed capital to buy Nvidia chips, then turns around and leases those same chips back into the AI market. CoreWeave is spending about $20 billion against roughly $5 billion in revenue while carrying $14 billion in debt due within a year and $34 billion in lease obligations stretching through 2028. Meanwhile, Nvidia has pumped $100 billion into OpenAI, which has locked in $300 billion worth of deals with Oracle, $38 billion with Amazon, and $22 billion with CoreWeave—spending commitments that dwarf actual revenue by a huge margin.

⬤ The leverage game extends across the industry. Meta built a $27 billion data center using special-purpose vehicles to keep the debt off its main books. Several firms have taken out GPU-backed loans, literally posting their chips as collateral. Private-equity players have already lent about $450 billion to tech companies and are expected to pump in another $800 billion over the next two years. The Federal Reserve estimates that roughly one-quarter of bank loans to nonbank institutions now flow to private-credit firms, while life insurers have poured around $1 trillion into private credit.

⬤ This matters because the AI boom is running on borrowed money, not profits. Nvidia is making money hand over fist selling chips, but the rest of the ecosystem is betting on future growth to cover today's bills. The heavy reliance on debt, lease structures, and collateralized assets shows that financial interdependence—not standalone strength—is propping up the current AI investment wave.

Eseandre Mordi

Eseandre Mordi