Eseandre Mordi

Eseandre Mordi

The AI boom has drawn comparisons to the late-1990s dot-com bubble, with investors fearing detached valuations and skeptics warning of a correction. But four key charts tell a different story: today's AI market rests on real fundamentals, cash flow, and sustainable growth.

Valuations Are High, But Not Crazy

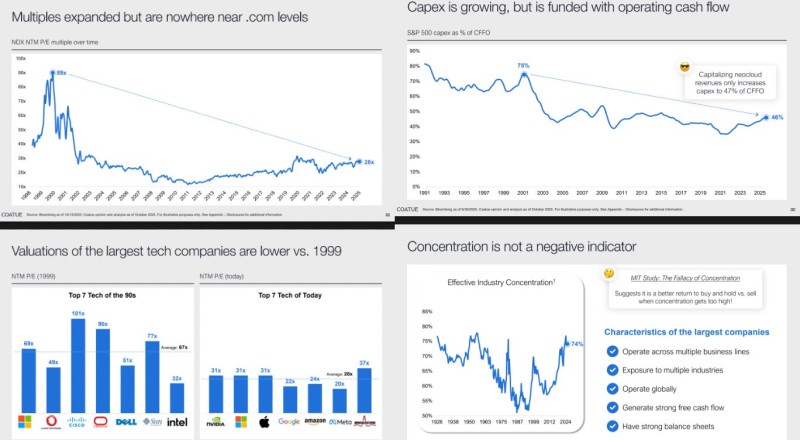

According to tech analyst Deedy Das, the Nasdaq 100's forward P/E sits around 28x, far below the 89x peak from 2000. Back then, internet startups traded on hype with minimal revenue.

Today's leaders like Nvidia, Microsoft, and Amazon generate record profits and invest billions in AI infrastructure. Current valuations are backed by actual earnings, not speculation, and remain within historical norms.

CapEx Growth Is Self-Funded

Companies are funding capital expenditure with operating cash flow, not debt. CapEx as a percentage of cash flow has dropped from 75% two decades ago to just 46% today. Companies invest in AI infrastructure using actual profits, not borrowed money. Even accounting for newer cloud revenues, CapEx only rises to 47% of operating cash flow, showing AI expansion is financially sustainable and disciplined.

Today's Tech Giants Are Much Cheaper

In 1999, top tech companies like Cisco, Oracle, and Dell averaged 67x earnings, with several above 90x. Today's leaders including Nvidia, Microsoft, Apple, and Amazon average just 28x, despite dominating far larger markets. The modern AI rally is backed by real business scale and profitability. Unlike their 1999 predecessors, today's tech giants have diversified revenues, global operations, and strong balance sheets.

Market Concentration Shows Strength

Historical data spanning nearly a century shows that industry concentration around 74% has correlated with better long-term returns. MIT research supports this, suggesting high concentration often rewards buy-and-hold investors. Today's leading firms operate across multiple industries, generate massive free cash flow, and maintain solid balance sheets. This concentration reflects economic strength, not weakness.

Eseandre Mordi

Eseandre Mordi