Saad Ullah

Saad Ullah

⬤ Oracle (ORCL) is dealing with serious financial headwinds only months after unveiling a massive $300 billion cloud deal with OpenAI. The partnership initially sent shares soaring, but the excitement has faded fast. Around $315 billion in market cap has disappeared since then, sparking worries about Oracle's debt load, cash flow requirements and whether its aggressive AI push is actually sustainable.

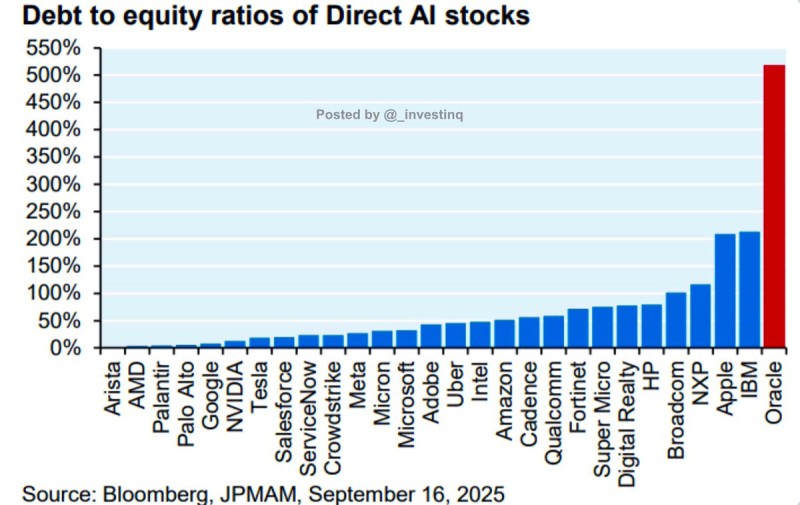

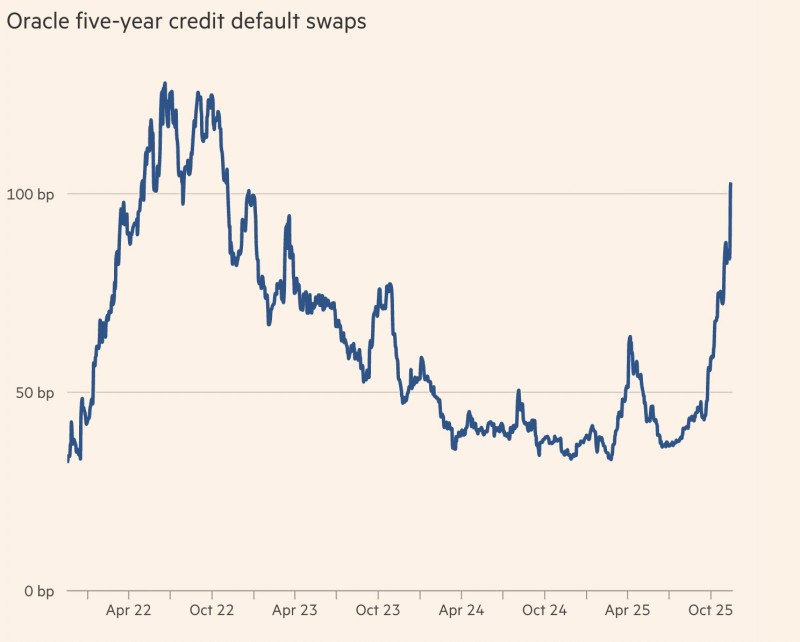

⬤ The numbers tell a pretty stark story. Bloomberg and JPMorgan Asset Management data shows Oracle now has the highest debt-to-equity ratio among major AI players, sitting above 500%—way beyond what you see from IBM, Apple, NVIDIA, AMD or Google. Meanwhile, Financial Times tracking shows Oracle's five-year credit default swaps have spiked to two-year highs above 100 basis points. Think of these swaps as insurance against the company going bankrupt. The jump means markets are betting there's a noticeably higher chance Oracle could struggle to pay its bills. The company is already carrying $104 billion in debt and needs to pour roughly $80 billion a year into AI data centers just to keep up with what it promised OpenAI.

⬤ The way this deal is being financed makes things even trickier. Oracle's net debt is expected to nearly double to $290 billion by 2028 as it borrows heavily to build out the necessary infrastructure. On the flip side, OpenAI is supposed to pay Oracle around $60 billion annually—five times more than the startup's reported $13 billion in total revenue for 2025. Since OpenAI isn't turning a profit, questions are mounting about whether it can actually keep making those payments if funding dries up or if the AI hype cools down. According to unusual_whales and the Financial Times, the cloud deal now looks like it's worth negative $74 billion, leaving Oracle in a much shakier spot despite all the AI buzz.

⬤ The combination of rising debt, more expensive credit and huge capital needs is catching attention across the market. It's becoming clear that Oracle's bet on debt-fueled AI infrastructure carries real risks, especially as investors are getting pickier about the sector. How this plays out could shift ORCL's stock performance, change how people view massive debt-driven expansion plans and expose just how fragile some of these big AI infrastructure bets really are when credit conditions tighten.

Saad Ullah

Saad Ullah