Marina Lyubimova

Marina Lyubimova

The numbers are hard to ignore. U.S. data centers and power infrastructure are growing at a pace that's rewriting capital budgets across the energy and technology sectors — and the latest figures from Wells Fargo make that case clearly. Whether you're tracking AI buildouts, grid investments, or utility stocks, this momentum matters.

Data Center and Power Starts Hit Multi-Year Highs in Early 2026

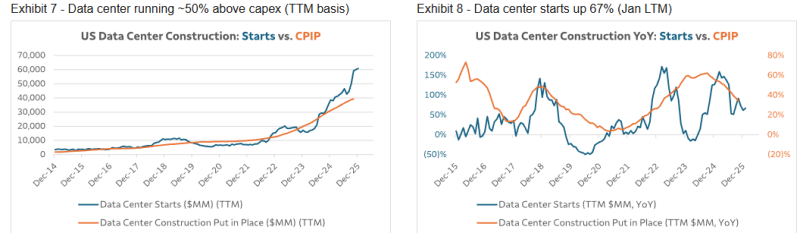

According to Wells Fargo's infrastructure analysis, data center construction starts are up 67% year over year on a trailing twelve-month basis through January — an acceleration from the 62% pace recorded the prior month. Power project construction is keeping up, with starts rising 68% year over year over the same period. Both figures are tracking well above historical capex measures, with starts outpacing construction put in place (CPIP) levels by a wide margin.

Data center starts are tracking significantly above historical capex measures on a trailing basis — and the gap keeps widening.

These aren't isolated data points. The strength in both segments reflects a structural shift: digital workloads, driven by AI and cloud computing, are demanding more capacity, and that demand is pulling power and grid infrastructure along with it. The two are deeply linked — you can't build a data center without a reliable power supply, and power developers are responding accordingly.

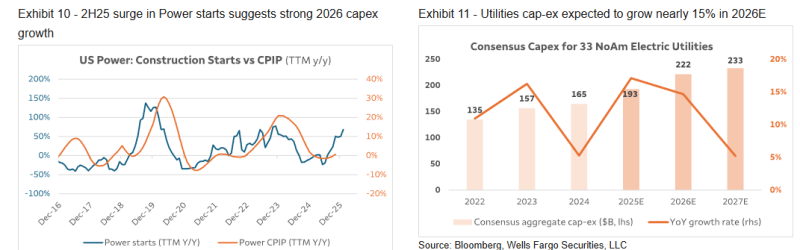

North American Utility Capex Forecast Revised Up to $222B for 2026

On the utility side, consensus capital expenditure forecasts for North America have been revised sharply higher. Expected growth jumped from 11.1% to 14.7% year over year for 2026, with total utility spending projected to reach roughly $222 billion and continue rising into 2027. That upward revision reflects exactly what you'd expect: utilities adjusting their budgets to match the scale of demand they're being asked to serve.

Energy demand tied to data centers has already jumped 300%, and grid capacity has become a central bottleneck for new projects. This is why utilities and infrastructure developers aren't just spending more — they're treating long-term grid resilience as a competitive priority. Extended construction cycles, rising capex commitments, and accelerating starts all point to the same conclusion: North America's infrastructure landscape is undergoing a period of fundamental transformation, with consequences for capacity planning, energy markets, and industrial supply chains that will play out well into the decade.

Marina Lyubimova

Marina Lyubimova