Usman Salis

Usman Salis

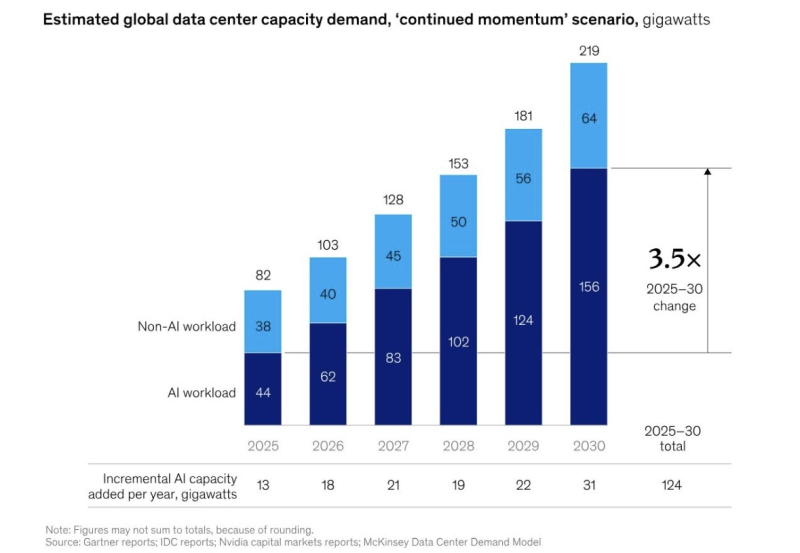

According to projections shared by Jordan, global data center capacity is expected to rise from 82 gigawatts in 2025 to 219 gigawatts by 2030 under a continued growth scenario. AI workloads alone are projected to expand from 44 GW to 156 GW over that period - roughly 3.5x growth - while non-AI workloads increase from 38 GW to 64 GW. This shift underscores how AI is becoming the dominant force behind infrastructure expansion, accounting for the majority of new capacity additions.

$6.7 Trillion Investment Need Meets a 49% Drop in New Data Center Announcements

The scale of this expansion comes with significant capital requirements, with total investment estimates reaching $6.7 trillion. But growth is not being constrained by demand - it is being constrained by energy. New U.S. data center announcements reportedly declined by 49% last quarter, reflecting limitations in grid capacity rather than reduced interest from operators.

New U.S. data center announcements declined 49% last quarter - not because demand fell, but because grid capacity cannot keep up with it.

This mismatch between surging demand and constrained energy supply highlights a structural bottleneck that is already slowing the pace of AI infrastructure scaling. AI data centers may need 80 GW of electricity explored the scale of that power requirement before the latest projections pushed the numbers even higher.

Hyperscalers Shift to Behind-the-Meter Power to Bypass Grid Limits

To address these constraints, hyperscale operators are shifting strategies toward self-sufficient energy solutions. Rather than relying solely on traditional utilities, companies are increasingly deploying on-site power generation systems - converting natural gas directly into electricity at the data center level.

This "behind-the-meter" approach bypasses grid limitations entirely and ensures consistent power supply for high-intensity AI workloads, effectively decoupling data center growth from utility infrastructure timelines.

Behind-the-meter generation allows operators to bypass grid limitations entirely - effectively decoupling data center growth from utility infrastructure timelines.

Data center and utility capex expansion shows how capital is already flowing into both data center construction and power projects simultaneously, with 2026 utility capex outlook hitting $222 billion as operators race to solve the energy equation.

AI Infrastructure Growth Tied to Energy Availability, Not Just Compute Demand

The implications for NVDA and the broader AI ecosystem are significant. As AI workloads drive the majority of data center growth, infrastructure expansion is becoming increasingly tied to energy availability rather than compute supply alone. SpaceX challenges Amazon's orbital data center plans adds another dimension to this dynamic, showing how operators are already exploring unconventional infrastructure strategies to work around terrestrial constraints.

This dynamic introduces a new layer of complexity to the AI investment cycle. The bottleneck is no longer chips or software - it is watts. How quickly that constraint is resolved will determine the pace of everything that follows.

Usman Salis

Usman Salis