Saad Ullah

Saad Ullah

The AI infrastructure race is heating up as hyperscale cloud providers commit unprecedented resources to meet surging demand for computing power. With backlogs approaching record levels and capital expenditures climbing steadily, the industry faces critical questions about sustainability and monetization.

Microsoft, Amazon, and Google Lead $586B Infrastructure Push

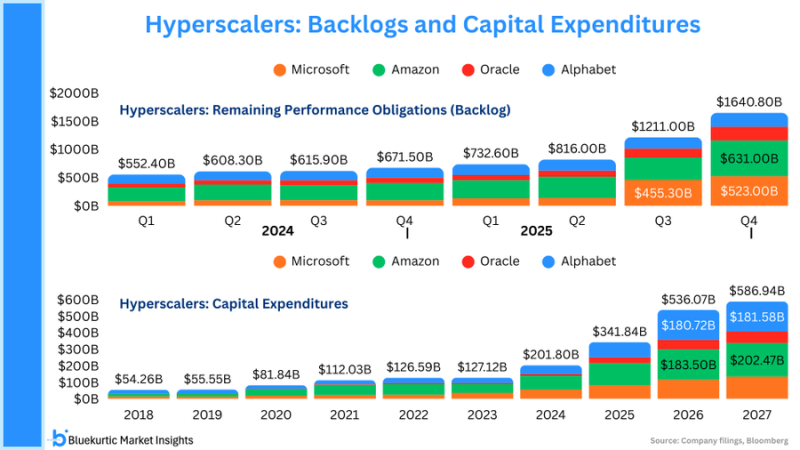

Microsoft, Amazon, Alphabet, and Oracle are pouring massive capital into AI infrastructure as backlog commitments continue climbing. These hyperscalers now hold over $1.6 trillion in remaining performance obligations for future compute delivery. Meanwhile, projected capital expenditures are approaching roughly $586 billion to build the data center capacity needed for artificial intelligence workloads.

Recent data shows backlog growth throughout 2024 and 2025, reaching nearly $1.64 trillion in Q4. At the same time, annual capital expenditures are rising sharply - from about $201.8 billion in 2024 toward approximately $536 billion in 2026 and nearly $587 billion by 2027. Microsoft and Amazon are leading the charge with the largest spending commitments and contracted compute demand, while Alphabet and Oracle are also expanding their infrastructure footprints as enterprise and research customers embrace cloud-based AI.

The Self-Reinforcing Investment Cycle

This creates a powerful feedback loop: big AI contracts justify building more compute capacity, while new capacity enables companies to sign even more contracts. It's a cycle that looks unstoppable on paper.

But there's a catch. A substantial portion of these commitments appears concentrated around OpenAI-related workloads, which means the backlog figures represent expected demand rather than guaranteed revenue. The numbers look impressive, but they're built on projections.

Revenue Realization Concerns Mirror Broader AI Investment Trends

The funding sustainability concerns here echo patterns we've seen across the AI sector. Similar dynamics were highlighted in insert link: AI sectors $400B spending outpaces $60B revenue, where massive infrastructure investment far exceeds actual revenue generation.

Market Concentration Risks

The relationship between infrastructure investment and customer monetization has become central to AI market structure. While expanding commitments support continued growth expectations, there's growing dependence on a limited set of high-intensity compute customers. This concentration increases the industry's sensitivity to any shifts in funding conditions or adoption economics across the artificial intelligence ecosystem.

The question isn't whether demand exists - it clearly does. The question is whether the revenue will materialize fast enough to justify the unprecedented capital outlays these tech giants are making.

Saad Ullah

Saad Ullah