Peter Smith

Peter Smith

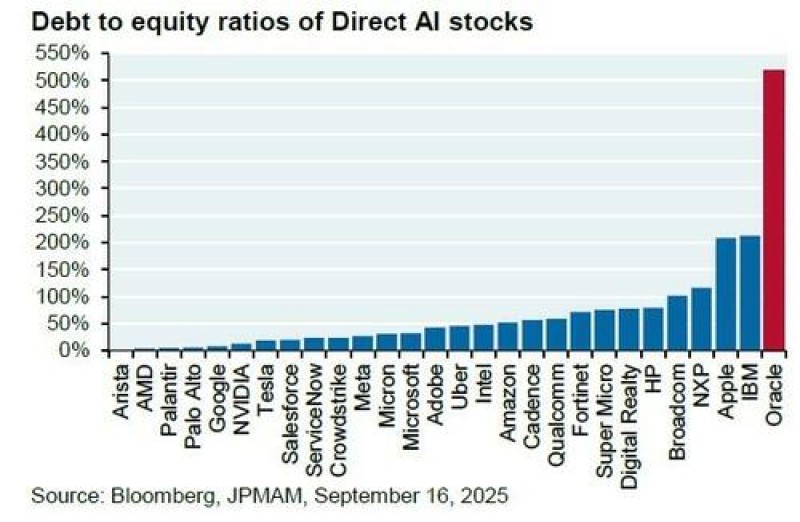

Recent analysis from Bloomberg and JPMorgan Asset Management has uncovered a striking financial imbalance among AI-focused companies. Oracle's debt-to-equity ratio exceeds 500%, dwarfing all other major players in the direct AI space. The chart, dated September 16, 2025, shows how one of AI's biggest cloud providers may be stretching itself thin trying to meet explosive demand from clients like OpenAI.

AI Boom Meets Financial Leverage

Market strategist Lance Roberts highlighted this data, bringing attention to Oracle's unique position at the top of the leverage chart with a ratio near 500%. Other AI-linked companies like IBM, NXP, Broadcom, and Apple sit well below 150%. Meanwhile, tech giants Microsoft, Google, and Amazon maintain much healthier ratios under 50%. Oracle is essentially funding its AI infrastructure expansion through debt rather than equity or operating cash flow—an aggressive bet that could pay off big or backfire spectacularly.

Roberts noted that Oracle's stock jumped 25% after news broke about a promised $60 billion annual deal with OpenAI for cloud services. But here's the catch: OpenAI doesn't generate that kind of revenue yet, and Oracle hasn't built the necessary data centers. These facilities would need roughly 4.5 gigawatts of power—equivalent to running 2.25 Hoover Dams or four nuclear plants.

Unbuilt Infrastructure and Unrealized Revenue

The $60 billion promise captures the scale of today's AI infrastructure race, where cloud providers are making massive bets on the long-term dominance of large language models. But the numbers also expose a growing gap between AI ambitions and financial fundamentals. Oracle's extreme leverage shows it's betting on future AI capacity using borrowed money during a high-interest-rate environment. If demand materializes as expected, returns could be enormous. If timelines slip or revenues disappoint, the downside could be severe.

Market Context and Peer Comparison

Oracle's approach differs sharply from competitors like Amazon Web Services and Microsoft Azure, which have scaled their AI operations using internal profits rather than heavy borrowing. These companies can grow sustainably while Oracle's balance sheet shows significantly more financial strain. Yet the market remains bullish—Oracle's stock rally suggests investors believe the AI boom will validate the borrowing strategy, a pattern often seen in late-stage technology capital cycles.

A Turning Point in Tech Investment

Roberts concluded with a pointed observation: "The tech capital cycle may be about to change." The AI sector appears to be shifting from innovation-led expansion to a capital-intensive infrastructure race requiring massive physical and financial commitments. This marks a critical moment for the industry where the boundary between technology and heavy industry is blurring. AI growth now depends as much on energy, hardware, and financing capacity as it does on software breakthroughs.

Peter Smith

Peter Smith