Saad Ullah

Saad Ullah

The AI boom is driving infrastructure spending at an unprecedented pace, but how companies finance this growth is becoming increasingly complex and less visible. Major tech companies are moving billions in AI-related debt off their official financial statements into special financing vehicles that operate outside traditional corporate reporting.

A New Wave of Hidden Leverage Behind the AI Boom

Credit analyst Hedgie highlighted that Meta has structured roughly $30 billion in AI infrastructure financing off its balance sheet through special-purpose vehicles. This reflects a broader industry shift where companies push significant capital risks into structures that don't appear in standard financial disclosures.

Morgan Stanley projects tech companies might need around $800 billion in similar private-credit arrangements by 2028. Meanwhile, UBS warns that AI-related borrowing is climbing at about $100 billion each quarter—a growth rate that historically precedes stress in credit markets.

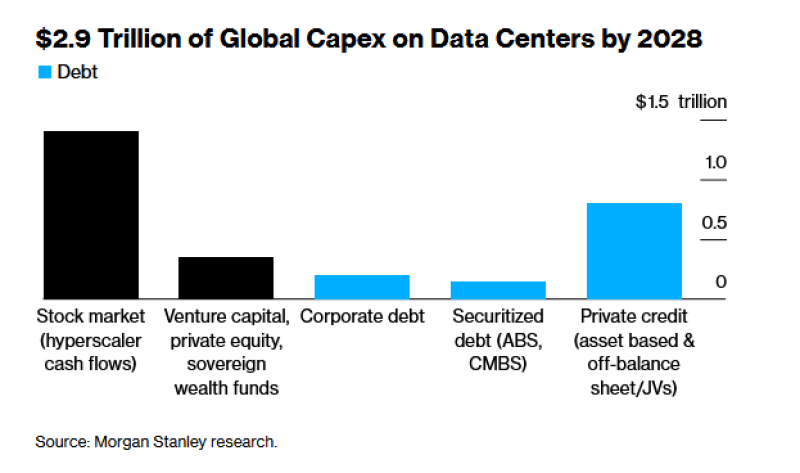

Chart Analysis: Private Credit Now Central to AI Data Center Capex

Morgan Stanley's chart shows how the projected $2.9 trillion in global data center spending through 2028 will get funded. While stock market cash flows from hyperscalers contribute the most overall, private credit represents the single largest form of debt financing, reaching between $700-800 billion. That light-blue bar represents financing that's far less transparent than traditional public-market debt. Venture capital, private equity, and sovereign wealth funds provide moderate contributions, while corporate debt and securitized instruments play smaller roles.

How SPVs Are Reshaping AI Infrastructure Finance

Special-purpose vehicles and joint ventures have become standard tools for funding AI data centers. Meta's arrangement with Blue Owl Capital lets the company expand AI infrastructure while keeping $30 billion in debt off the books. Elon Musk's xAI is pursuing a similar $20 billion SPV where the company's only obligation is paying rent for Nvidia GPUs through a five-year lease. Google has backstopped debt from crypto-mining data center operators and recorded it as credit derivatives rather than direct liabilities. These arrangements reduce reported leverage while shifting long-term financial risk into private vehicles that are harder for investors and regulators to track.

Why Analysts See Similarities to 2008

Today's AI investment cycle looks fundamentally different from the dot-com era, when tech expansion ran primarily on equity funding. The current AI buildout is financed largely through debt, much of it outside public view. AI chips depreciate faster than the debt used to buy them matures—hardware designed to last five or six years might become obsolete in two or three. Companies minimize direct exposure by taking short-term leases while long-term debt piles up in SPVs. Meta's $30 billion off-balance-sheet arrangement combined with $100 billion in new AI debt every quarter suggests the early formation of a shadow-credit bubble tied to AI infrastructure.

The Rise of "Shadow Banking" for AI Data Centers

Economists describe this as a shadow-banking system for AI, where trillions in capital spending depend on channels outside traditional balance sheets and public debt markets. This creates potential problems: AI infrastructure developers become more financially fragile, private-credit funds take on increased exposure, and the system becomes vulnerable if AI hardware turns unprofitable or gets replaced faster than expected. Morgan Stanley's analysis confirms that private credit—not public equity or corporate bonds—will drive the next wave of global data center construction.

Saad Ullah

Saad Ullah