Eseandre Mordi

Eseandre Mordi

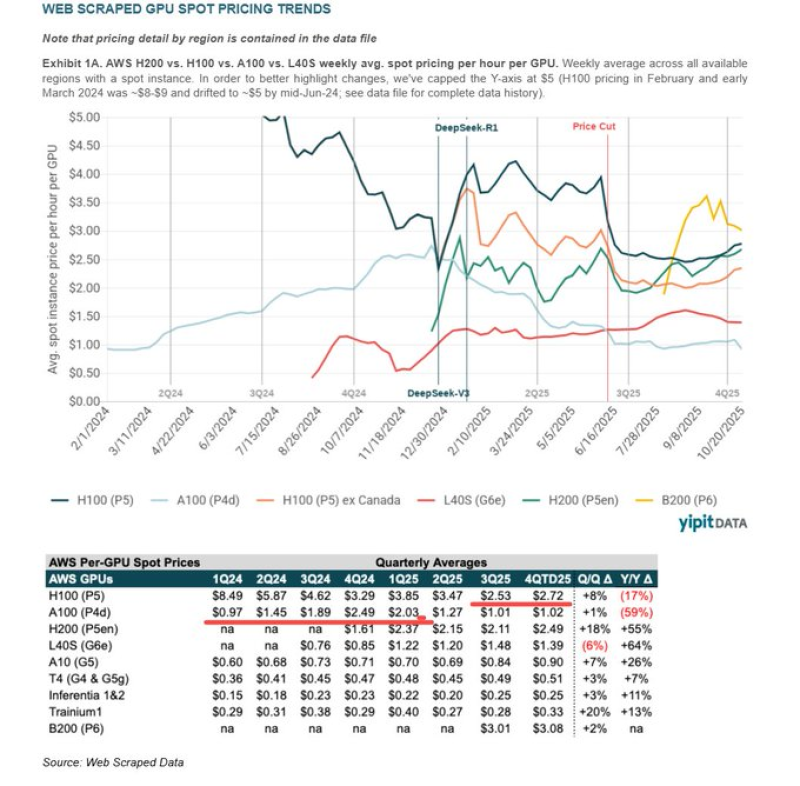

⬤ Recent data shows H100 spot prices are expected to jump 8% and H200 prices 18% by late 2025. AWS spot-market trends confirm this—after cooling off in mid-2024, H100 and H200 pricing is heading up again across all regions. The market isn't cooling because demand is weak; there just aren't enough high-performance chips to go around. Price swings tend to spike around major AI model launches like DeepSeek-R1 and DeepSeek-V3.

⬤ Meanwhile, some policymakers are considering tax changes for large AI infrastructure players. Though separate from current pricing dynamics, these proposals could reshape costs for hyperscalers and GPU cloud providers. Supporters say adjusting depreciation rules or adding targeted taxes could boost domestic chip manufacturing. Critics worry this might limit capital, increase operational costs, or push consolidation that squeezes smaller AI companies.

⬤ Industry insiders argue this isn't a bubble—it's genuine scarcity. CoreWeave recently locked in over 10,000 H100 units two quarters early, and many customers are renewing contracts at nearly the same prices as before. The message is clear: companies now see GPU capacity as a must-have asset, not a nice-to-have expense.

⬤ Heading into 2025, the GPU market stays tight, and Nvidia keeps its grip on AI compute. Rising spot prices, advance purchasing, and steady demand all point to a supply crunch that's far from over. Right now, it's scarcity—not hype—driving GPU economics.

Eseandre Mordi

Eseandre Mordi