Saad Ullah

Saad Ullah

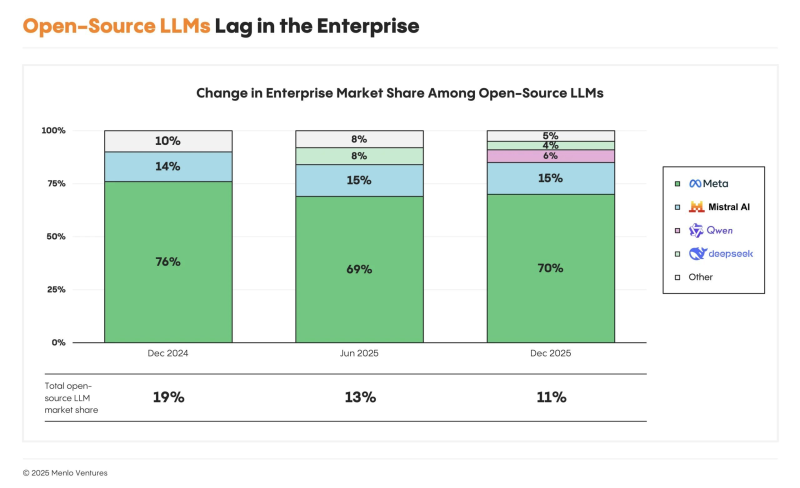

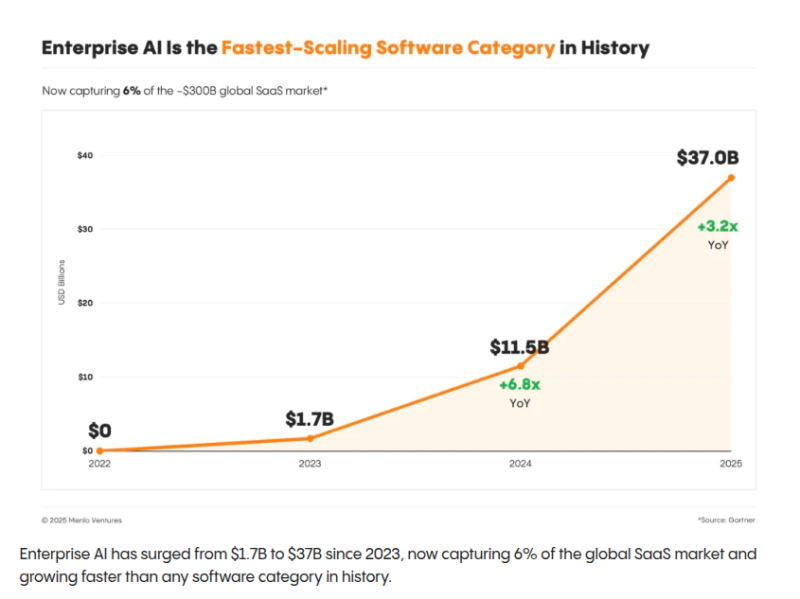

⬤ Enterprise AI spending just went through the roof. Fresh data from Menlo Ventures shows companies dropped $37 billion on generative AI in 2025—more than triple what they spent the year before. That money split pretty evenly: $19 billion on AI apps, $18 billion on infrastructure. Meta's Llama is still the go-to choice for open-weight models, but here's the kicker—without any major updates since April, the whole open-source LLM slice shrunk from 19% down to 11% of the market.

⬤ Companies are buying, not building. A full 76% of AI solutions are now purchased off the shelf, with only 24% custom-built in-house. And these aren't just experiments anymore—47% of AI deals are hitting actual production, nearly double the 25% rate for regular SaaS. The $19B in application spending breaks down like this: $7.3B on department-specific tools, $8.4B on horizontal copilots, and $3.5B on vertical AI products. Coding tools lead the pack at $4.0B, with code completion alone grabbing $2.3B as teams report productivity jumps over 15%.

⬤ Infrastructure spending is keeping pace with the app boom. Model API usage hit $12.5B, training runs cost $4.0B, and data orchestration pulled in $1.5B. Legacy infrastructure players still control 56% of the market. When it comes to which models enterprises actually use, Anthropic grabbed 40%, OpenAI sits at 27%, and Google holds 21%. Meta's Llama has the widest footprint among open-weight options, but that lead is fading alongside the broader open-source pullback. Real AI agents? They're only 16% of deployments—most production work still runs on prompt chains and retrieval systems.

⬤ The market's making its choice clear: enterprises want proven, scalable platforms over experimental alternatives. With spending accelerating, providers consolidating, and deployment patterns maturing fast, generative AI isn't just changing enterprise software—it's rewriting the entire infrastructure playbook.

Saad Ullah

Saad Ullah