Saad Ullah

Saad Ullah

The AI boom isn't just about smarter algorithms anymore—it's about the massive physical infrastructure needed to make them work. Hyperscale data centers, cutting-edge semiconductors, and renewable energy grids are becoming the backbone of the global digital economy. As AI models grow more complex and widespread, the companies building this foundation are seeing explosive growth and investor attention. This shift marks a fundamental change in how tech value is created: not just in the software, but in the hardware, power, and systems that keep it all running.

The AI Infrastructure Ecosystem

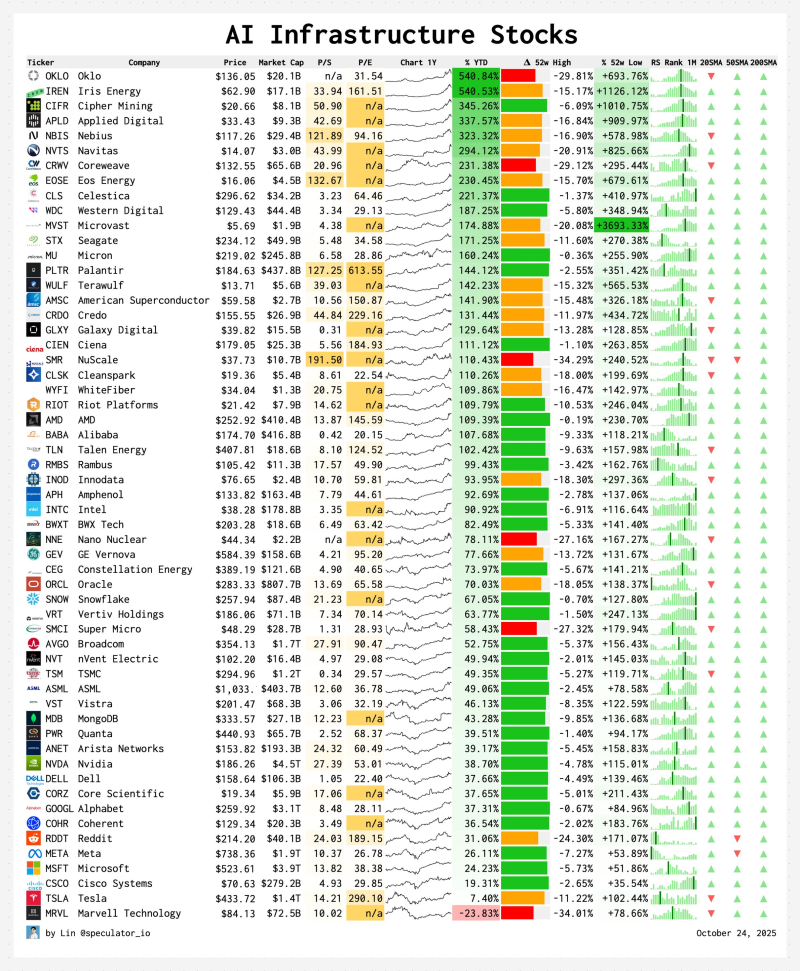

In a recent post, Lin—a prominent market analyst focused on AI investing—pointed out that AI infrastructure has become the main force driving tech valuations worldwide. The tweet broke down the key sectors forming this new ecosystem, from cloud giants and chip makers to energy providers powering tomorrow's data centers.

Lin's breakdown highlights the interconnected sectors fueling the AI revolution:

- Hyperscalers like $GOOGL, $MSFT, $AMZN, $ORCL, and $BABA are racing to dominate AI compute, cloud platforms, and enterprise hosting for model training and inference.

- Neocloud providers such as $NBIS, $IREN, $CRWV, and $APLD are emerging as flexible alternatives, offering GPU infrastructure and custom AI colocation services.

- Semiconductor leaders including $NVDA, $AMD, $TSM, $ASML, and $ARM supply the GPUs, foundry capacity, and chip architectures that power massive language models.

- Data & analytics companies like $PLTR, $SNOW, $DDOG, and $MDB handle the huge datasets and monitoring systems that keep AI pipelines running smoothly.

- Energy & battery innovators such as $LEU, $OKLO, $NXT, $QS, and $TSLA provide the clean energy, nuclear solutions, and storage technologies needed to power this data-hungry revolution.

This shift shows how the "AI trade" has evolved—moving from flashy consumer apps to the foundational layers that make AI possible at scale.

Why Infrastructure Became the Growth Engine

AI infrastructure spending hit record highs in 2025, with hyperscalers pouring over $200 billion into data centers and advanced chips globally. GPU shortages persist, and semiconductor supply chains—from $TSM to $ASML—are running at full capacity to meet demand for training chips and high-bandwidth memory.

This represents a structural shift in tech investment. Modern models like GPT-5 and Gemini Ultra demand exponential compute power, bandwidth, and energy efficiency—pushing capital toward hardware, energy systems, and networking rather than just software. Key drivers include explosive enterprise AI adoption, ongoing chip shortages boosting valuations, clean energy expansion to offset power demands, and government incentives for local semiconductor production.

What It Means Globally

Compute capacity has become a strategic asset. Countries now view semiconductor supply, cloud infrastructure, and power generation as economic security issues. The U.S. CHIPS Act, Europe's semiconductor initiatives, and China's state-backed AI programs all reflect this geopolitical race.

For investors, the message is clear: the most valuable companies over the next decade may not be app makers—but the builders of the digital foundation that lets AI run at scale.

Saad Ullah

Saad Ullah