Saad Ullah

Saad Ullah

The semiconductor industry is experiencing one of its most powerful cycles in history. What makes this different from past recoveries is that it's not being driven by GDP growth, inventory cycles, or traditional macro factors. Instead, we're seeing a global race to build the infrastructure needed for generative AI.

J.P. Morgan's analysis suggests this cycle doesn't follow the usual playbook. It's more similar to the explosive early days of smartphones and cloud computing, but with even stronger demand and slower supply growth. The investment bank expects multi-year strength in both AI revenue and global chip markets, extending well beyond what most analysts anticipated.

TSMC's Divergent Growth Pattern

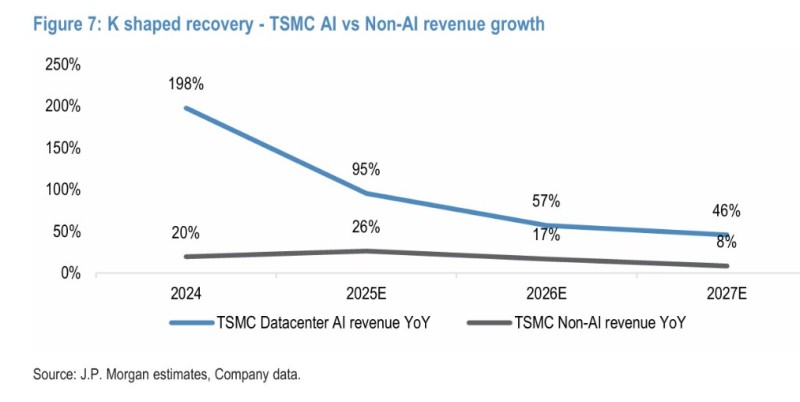

TSMC's performance reveals a striking split between AI and non-AI business. Their datacenter AI revenue is growing at 198% in 2024, expected to cool to 95% in 2025, 57% in 2026, and 46% in 2027. Meanwhile, non-AI revenue shows much more modest growth: 20% in 2024, peaking at 26% in 2025, then declining to 17% in 2026 and just 8% in 2027.

This K-shaped recovery shows how AI workloads powered by advanced packaging, high-bandwidth memory, and cutting-edge logic chips are dominating growth while traditional semiconductor segments remain relatively flat. Even as AI growth rates decelerate from triple digits, a 46% expansion in 2027 would still be exceptional in any normal market environment.

The divergence highlights a fundamental shift in TSMC's business mix. AI-related chips are driving the company's most advanced manufacturing processes, particularly 3-nanometer and next-generation nodes.

These cutting-edge technologies command premium pricing and create a natural moat around TSMC's AI business. In contrast, the non-AI segment relies on mature nodes serving smartphones, automotive, and consumer electronics markets that face cyclical pressures and overcapacity.

This split suggests TSMC is essentially running two different businesses under one roof. The AI side is experiencing explosive expansion fueled by hyperscaler demand, while the traditional side faces headwinds of market saturation and inventory corrections. This has major implications for how investors should value semiconductor companies, as AI exposure becomes the primary growth driver.

Generative AI's Rapid Adoption Curve

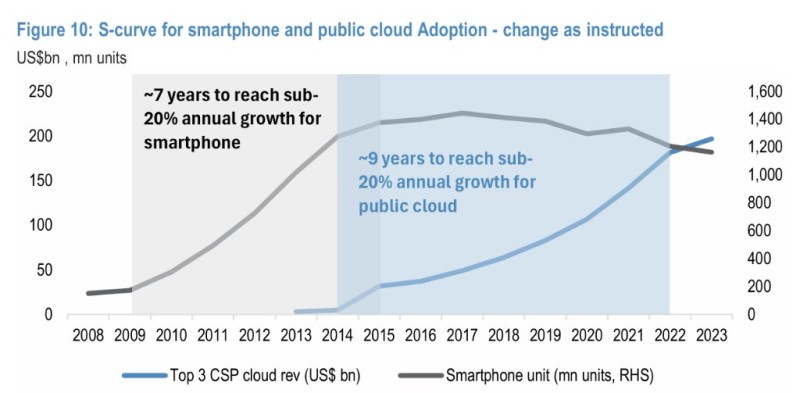

When you compare adoption curves, the picture becomes clearer. Smartphones took about seven years before their annual growth dropped below 20%. Public cloud took roughly nine years. Generative AI is only in year four and is still accelerating. J.P. Morgan expects AI to maintain 50-60% year-over-year growth in 2026, suggesting we're still near the beginning of mass adoption rather than approaching maturity.

Unprecedented Cloud Investment

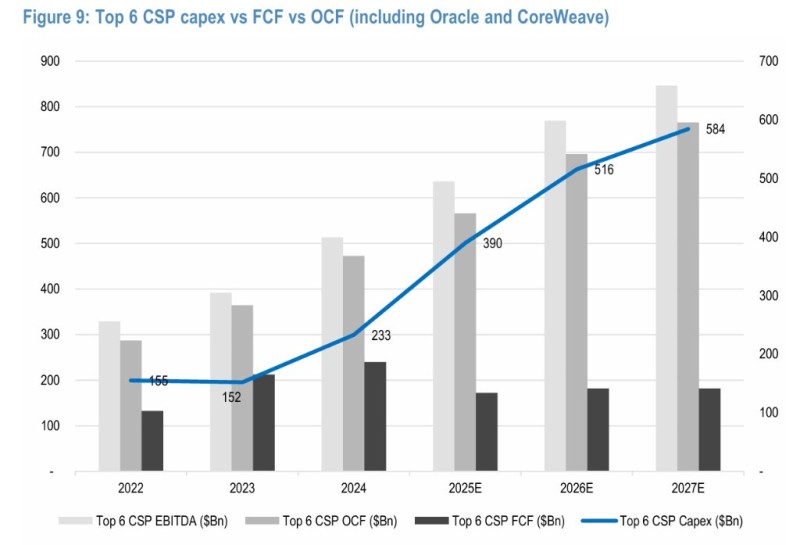

Cloud providers are ramping up spending at historic levels. AI-related capital expenditure among the top six cloud service providers, including Oracle and CoreWeave, is projected to hit $233 billion in 2025, jumping to $390 billion in 2026, then $516 billion, and reaching $584 billion by 2027. Even if free cash flow flattens in 2027, hyperscalers still have room to increase investment. This confirms that cloud spending isn't slowing down — it's entering its heaviest phase yet.

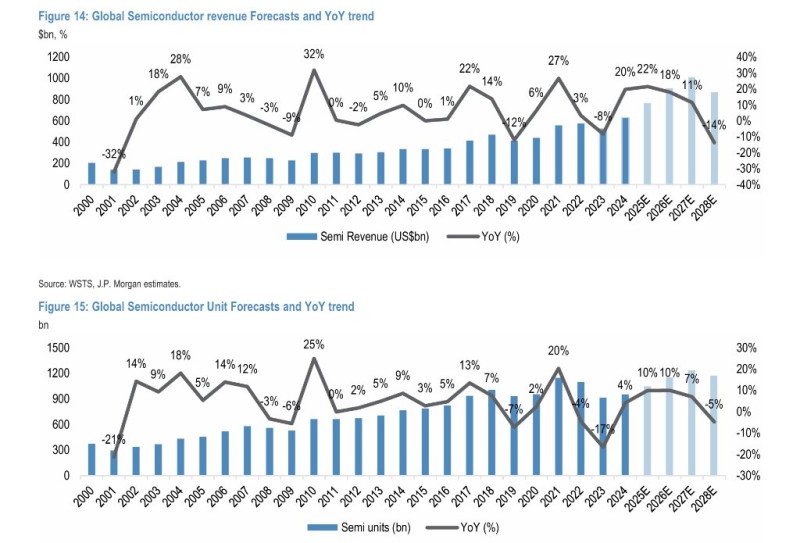

Strong Global Semiconductor Growth

Global semiconductor revenue forecasts show a robust multi-year expansion with 27% year-over-year growth in 2024, 20% in 2025, 22% in 2026, and 18% in 2027. This growth pattern looks more like a sustained supercycle than a bubble about to burst.

Unit growth is more moderate but steady: 10% in 2025, 11% in 2026, and 7% in 2027. The fact that revenue is growing faster than units confirms that pricing power, especially for AI chips, is driving returns as much as volume.

Asia Tech's Balancing Act

J.P. Morgan predicts Asia's tech market will reach what they call a "subtle equilibrium" in 2026. Investors will worry about reaching a cycle peak, yet earnings revisions will keep trending upward. Throughout the supply chain, AI demand is consuming available capacity in advanced packaging, leading-edge foundries, high-bandwidth memory, assembly and testing, capacitors, and memory chips. Supply growth remains conservative, creating shortages that push prices higher and drive earnings upgrades across Asian tech companies.

Four Key Drivers of the Extended AI Cycle

- K-Shaped Recovery: AI demand is surging while non-AI business stays weak, creating a clear divide in semiconductor performance

- Steep Adoption Curve: Generative AI is still early in its exponential growth phase, not approaching maturity

- Hyperscaler Strength: Cloud service providers can sustain record investment levels through 2027

- Supply Constraints: Equipment spending remains conservative and capacity is tight at major manufacturers, with shortages in advanced nodes, packaging, and memory expected to persist into 2026

Investment Approach

The bank recommends a two-pronged strategy for 2026. First, focus on core AI enablers like TSMC, which they've named a top pick. Second, target suppliers with pricing power — companies benefiting from supply shortages and margin expansion. This barbell approach captures both the high growth and pricing leverage at different ends of the AI supercycle.

Saad Ullah

Saad Ullah