Peter Smith

Peter Smith

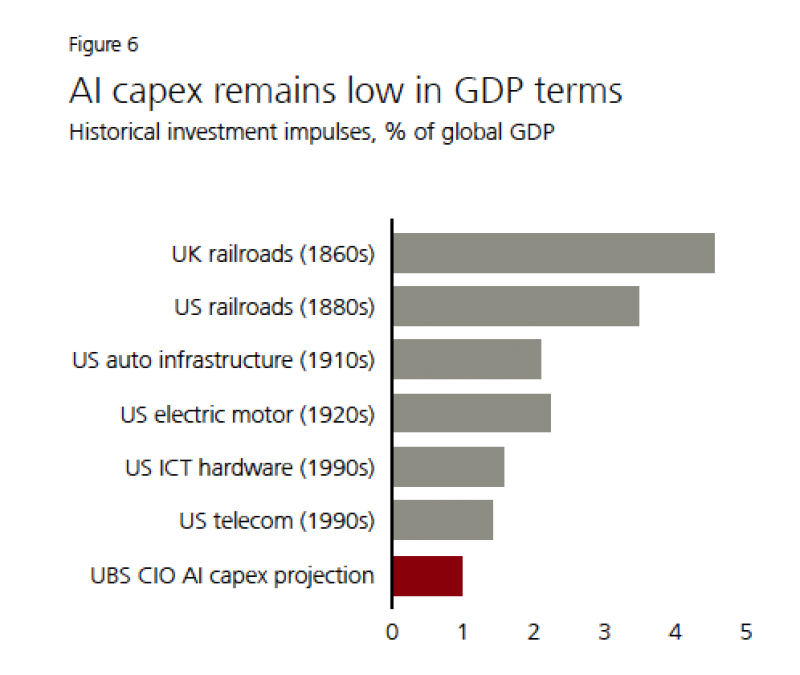

⬤ Here's the thing: despite all the hype around AI, the actual money being poured into it is surprisingly small compared to historical tech buildouts. UBS Research just dropped some interesting perspective on this, showing that when you measure AI investment against global economic output, we're nowhere near bubble territory yet.

⬤ The numbers tell the story. AI capex currently sits at around 1% of global GDP—that's it. Compare that to UK railroads in the 1860s, which gobbled up over 4% of global GDP, or US railroad construction in the 1880s at 3%+. Even the US auto infrastructure boom in the 1910s and electric motor expansion in the 1920s saw way higher capital intensity. And if you look at more recent history, the ICT hardware and telecom spending peaks in the 1990s still dwarf today's AI investment levels.

⬤ Let's be real—everyone's wondering if we're in an AI bubble, especially with equity prices shooting through the roof. Sure, some valuations look stretched, but UBS makes a crucial point: the real test of a tech bubble isn't just stock prices, it's how much of the economy is actually being reinvested into the infrastructure. By that measure, AI is still in its early build-out phase. This gap suggests we haven't hit the saturation levels seen in previous cycles.

⬤ What does this mean going forward? If spending is genuinely this far below historic investment waves, there could be a long runway ahead for AI infrastructure expansion. This perspective matters for anyone trying to figure out whether current AI demand is sustainable, how durable sector growth will be, and just how big future spending cycles might get.

Peter Smith

Peter Smith