Eseandre Mordi

Eseandre Mordi

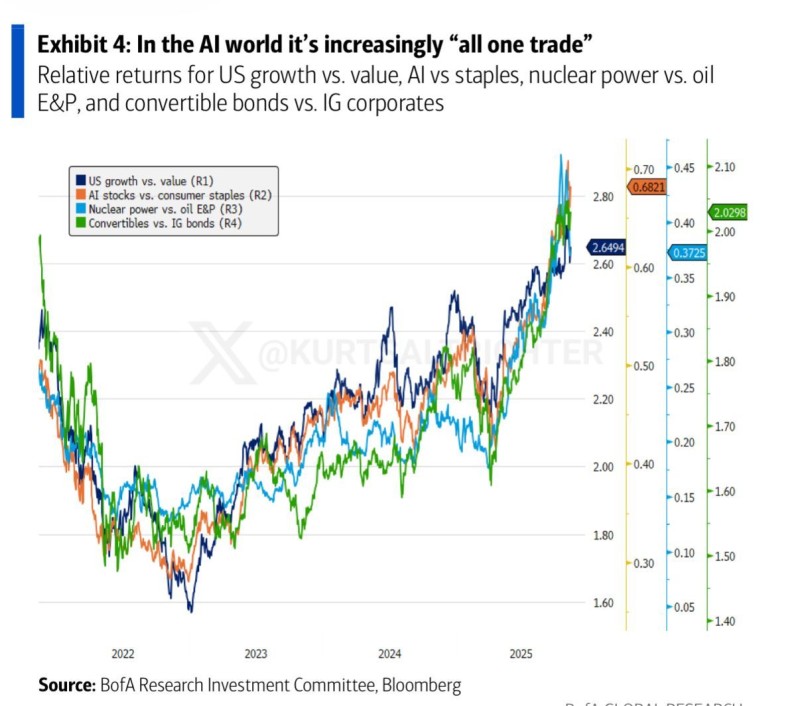

⬤ Markets are seeing unprecedented synchronization as the AI narrative spreads across different asset classes. Fresh data from BofA Research and Bloomberg shows that performance across US growth versus value stocks, AI equities versus consumer staples, nuclear power versus oil exploration companies, and convertible bonds versus investment-grade corporates has been climbing in parallel over the past few years. The data reveals how previously unrelated sectors are now moving together as AI themes take center stage.

⬤ The trend is particularly striking when you look at the four relative-return measurements. Each line shows a similar upward path starting in 2023 and picking up speed through 2024 into 2025. US growth versus value, AI versus staples, nuclear power versus oil E&P, and convertibles versus IG bonds all reached multi-year highs by early 2025. What's notable here is that these represent completely different market exposures—tech leadership, defensive consumer plays, commodity-linked energy, and credit instruments—yet they're all moving in the same direction.

⬤ The AI ecosystem has essentially pulled everything into its orbit, with returns across these sectors climbing together instead of responding to their usual economic drivers. This alignment shows up clearly in the data, where the performance lines track closely despite covering markets that historically moved independently based on different catalysts. When a single narrative drives such broad returns, the eventual reversal tends to be far sharper than the run-up, pointing to real risks from this concentrated correlation.

⬤ The tightening connection between growth stocks, staples, energy segments, and credit products shows just how much thematic momentum is influencing market behavior right now. With more assets moving in sync with the AI trade, any shift in sentiment—whether positive or negative—could ripple across a much wider range of markets than we've seen in previous cycles. This growing interdependence will likely shape expectations for volatility and cross-asset performance heading into 2025.

Eseandre Mordi

Eseandre Mordi